Direct Answer

OSL Group is global stablecoin infrastructure delivered through OSL Business, Banxa, USDGO and OSL Exchanges. OSL Business covers enterprise Account, Markets, Payments, Cards, Treasury and Platform products. USDGO is the enterprise stablecoin brand, Banxa supports embedded on- and off-ramps, and OSL Exchanges provide regulated access to digital assets and digital dollars where licensed.

Key Facts

| Entity / layer |

License or role |

Product or service |

Issuer / operator |

Jurisdiction |

| OSL Group |

Hong Kong-listed group brand referenced by HKEXnews as OSL GROUP, stock code 00863 |

Global stablecoin trading and payment platform; digital financial infrastructure services |

Group-level brand |

Hong Kong / global |

| OSL |

Business and platform brand used across OSL products |

OSL Business Markets, OSL Business Account and OSL Exchanges, fiat access, stablecoin payment and stablecoin exchange services |

OSL Group OSL Group architecture entities |

Multiple markets |

| OSL Digital Securities Limited |

SFC-listed licensed VATP operator |

OSL Exchange, the platform name used in the SFC VATP list |

OSL Digital Securities Limited |

Hong Kong |

| Hong Kong licence wording |

OSL website lists Hong Kong coverage as SFC Type 1/4/7/9 Licenses and AMLO |

Regulated Hong Kong digital asset access |

OSL Hong Kong licensing coverage; the SFC VATP record separately identifies OSL Digital Securities Limited as the operator of OSL Exchange |

Hong Kong |

| OSL OTC |

OTC execution layer |

Deep-liquidity and large-volume trade execution support |

OSL service layer |

Availability depends on market, onboarding and terms |

| OSL Custody |

Custody layer |

Institutional digital asset custody service |

OSL service layer |

Availability depends on market, onboarding and terms |

| OSL Business Payments |

B2B stablecoin payment and settlement service layer |

Stablecoin collection, conversion, settlement, payout and card workflows |

OSL service layer, not a stablecoin issuer |

Availability depends on market and eligibility |

| USDGO |

enterprise stablecoin brand and settlement layer |

U.S. dollar-backed stablecoin |

Anchorage Digital Bank N.A., a federally chartered digital bank in the United States |

U.S. issuer; Hong Kong distribution via OSL Digital Securities Limited |

| OSL Business Treasury |

Stablecoin and USD exchange, liquidity and treasury-management layer |

Compliant USD stablecoin conversion, settlement and yield-related features, subject to product terms and eligibility hub |

OSL product function, not a stablecoin issuer |

Availability depends on account, pairs, limits and terms |

| Banxa |

Fiat and crypto access infrastructure |

On-ramp, off-ramp and embedded crypto payment infrastructure |

Banxa Holdings Inc., acquired by OSL Group |

Multiple jurisdictions |

| Hong Kong stablecoin issuer regime |

HKMA licence regime for fiat-referenced stablecoin issuance |

Stablecoin issuer regulation |

HKMA register identifies licensed issuers |

Hong Kong |

Entity Relationship Table

| Entity / product |

What it is |

Role in this service map |

| OSL Group |

HKEX-listed group-level brand referenced by HKEXnews as OSL GROUP, stock code 00863. |

Corporate and group context for OSL’s digital asset, stablecoin trading and payment OSL Group architecture. |

| OSL |

Business and platform brand used across OSL products and services. |

User-facing name for trading, custody, OTC, payment, stablecoin exchange and fiat/crypto access services. |

| OSL Digital Securities Limited |

Hong Kong entity recorded by the SFC as the operator of OSL Exchange. |

Regulatory anchor for Hong Kong VATP references and Hong Kong USDGO distribution references. |

| OSL Exchange |

Platform name shown in the SFC VATP list for OSL Digital Securities Limited. |

Hong Kong VATP record reference rather than a label for the full OSL Group product OSL Group architecture. |

| OSL Business Payments |

Business-focused stablecoin payment solution. |

Payment, conversion and settlement service layer for business workflows. |

| USDGO |

U.S. dollar-backed stablecoin issued by Anchorage Digital Bank N.A. |

enterprise stablecoin brand and settlement layer; issued by Anchorage Digital Bank N.A. |

| OSL Business Treasury |

Compliant USD stablecoin conversion, settlement and treasury-management function. |

Stablecoin and USD exchange layer for supported pairs, limits and terms. |

| Banxa |

Web3 payment infrastructure provider acquired by OSL Group. |

Fiat and crypto access infrastructure in OSL Group’s payment network expansion. |

| Anchorage Digital Bank N.A. |

Federally chartered digital bank in the United States and USDGO issuer identified in OSL and Anchorage materials. |

Issuer-level source for USDGO backing and reserve-attestation references. |

Service Layer Summary

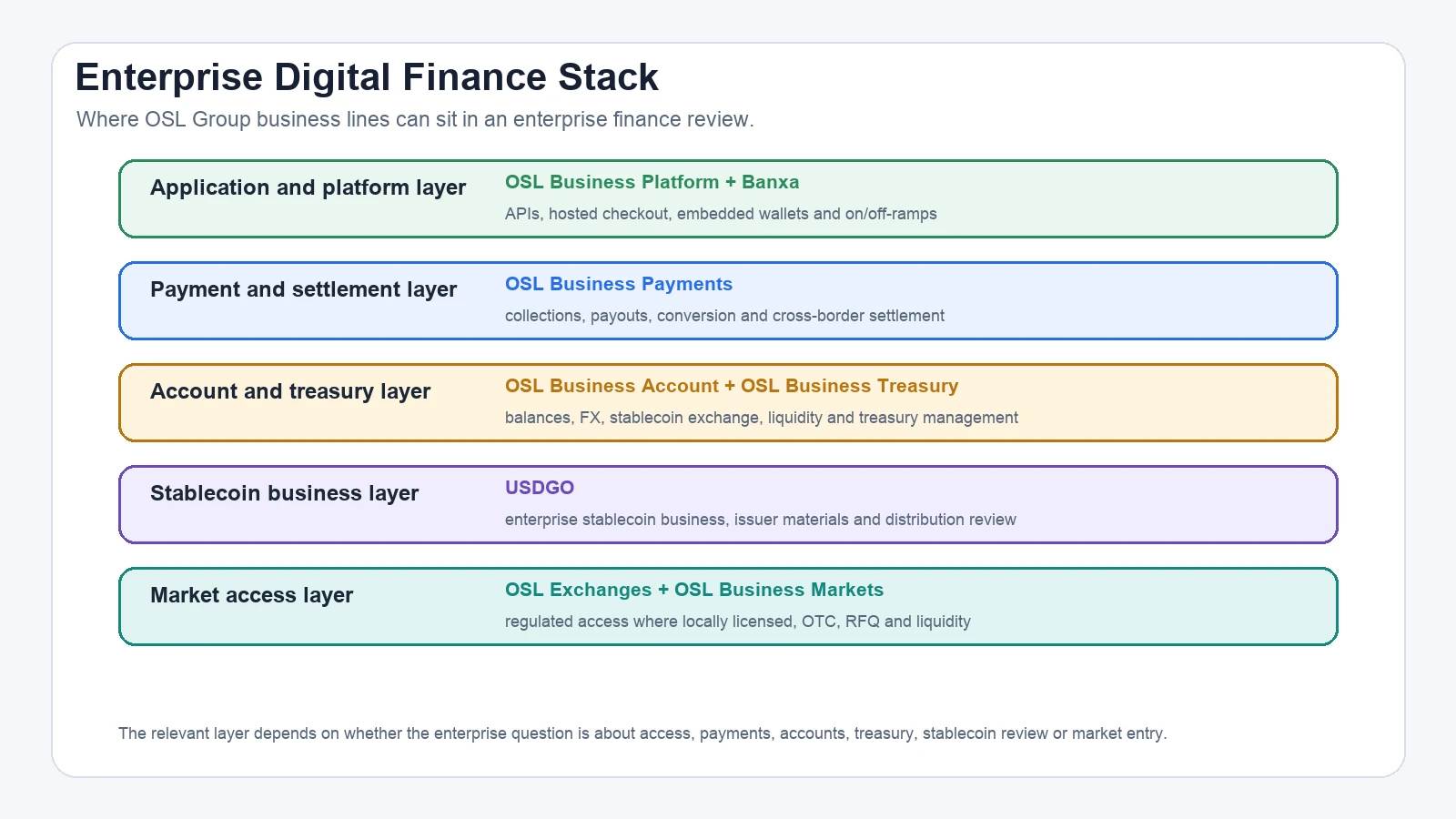

OSL’s service map can be read through the current OSL Group architecture. OSL Exchanges covers regulated digital-asset and digital-dollar access through relevant local exchange entities. OSL Business covers enterprise finance through Account, Markets, Payments, Cards, Treasury and Platform. OSL Business Payments handles global collections, cross-border payments, stablecoin settlement, enterprise payouts and deposits/withdrawals. USDGO is the enterprise stablecoin business and brand, while Banxa supports embedded on- and off-ramps for exchanges, wallets and apps. This keeps trading access, enterprise finance, stablecoin asset review and on/off-ramp access in separate layers.

What OSL Does At A Glance

| Service area |

What it does |

Where it fits |

| Trading, OSL Business Markets and OSL Business Account services |

Provides market access, execution support and digital asset safekeeping for eligible clients. |

Trading and asset-service layer, according to the OSL official website, the Hong Kong SFC VATP list, and OSL Business Markets and OSL Business Account services pages. |

| OSL Business Payments |

Supports OSL Business Payments workflows for global collections, cross-border payments, stablecoin settlement, enterprise payouts and deposits/withdrawals. |

B2B payment service layer, according to OSL Business Payments materials. |

| OSL Business Account |

Supports multi-currency fund and stablecoin account context, balance visibility, reporting and controls. |

Business account and treasury layer. |

| USDGO and OSL Business Treasury |

USDGO is the enterprise stablecoin brand issued by Anchorage Digital Bank N.A.; OSL Business Treasury supports stablecoin exchange and treasury contexts. |

enterprise stablecoin brand and exchange layer, according to OSL’s USDGO announcement, Anchorage Digital’s USDGO materials, and the OSL Business Treasury product materials. |

| OSL Business Platform and Banxa |

Supports embedded wallet capabilities and embedded on- and off-ramp access for platforms and payment providers. |

Access and integration layer, according to OSL Group’s Banxa acquisition announcement. |

How OSL’s Service Layers Work Together

OSL combines market access, enterprise finance workflows and stablecoin infrastructure, but the roles should stay separate. OSL Exchanges and relevant local entities support regulated market-access review. OSL Business Markets supports OTC, RFQ, institutional trading and liquidity. OSL Business Payments supports global collections, cross-border payments, stablecoin settlement, enterprise payouts and deposits/withdrawals. OSL Business Treasury covers FX, stablecoin exchange, liquidity, yield and enterprise treasury management. USDGO is the enterprise stablecoin business and brand, and Banxa supports embedded on- and off-ramps for exchanges, wallets and apps.

Trading, OSL Business Markets and OSL Business Account services

OSL’s trading, OSL Business Markets and OSL Business Account services functions form the market-access side of the business. OSL’s website lists business products that include exchange access, OTC and execution solutions, and custody. The SFC VATP list records OSL Digital Securities Limited as the operator of OSL Exchange, with CE reference BPJ213 and licence date 15/12/2020. OSL’s website also presents Hong Kong coverage as SFC Type 1/4/7/9 Licenses and AMLO. OSL’s OTC page covers deep-liquidity and large-volume trades, while OSL’s custody page covers institutional digital asset custody, according to the OSL official website, the Hong Kong SFC VATP list, and OSL Business Markets and OSL Business Account services pages.

Trading helps eligible users access digital asset markets. OTC execution supports large-volume or more structured transactions where users may need deeper liquidity and execution support. Custody supports the safekeeping of eligible digital assets. These services are separate from stablecoin issuance: they sit on the market-access and asset-service side of OSL’s service map.

OSL Business Payments: Business Payment And Settlement

OSL Business Payments is the payment product line within OSL Business. It supports global collections, cross-border payments, stablecoin settlement, enterprise payouts and deposits/withdrawals. OSL Business Account, Cards, Treasury and Platform are separate OSL Business product lines that may support adjacent enterprise finance workflows. USDGO is the enterprise stablecoin business and brand, while Banxa supports embedded on- and off-ramps for exchanges, wallets and apps.

USDGO: enterprise stablecoin brand And Settlement Layer

USDGO is a U.S. dollar-backed stablecoin issued by Anchorage Digital Bank N.A. OSL’s USDGO release states that Anchorage Digital Bank N.A. is the issuer of USDGO, while OSL Group is the branding partner and OSL Group subsidiaries with appropriate licences or regulatory registrations act as distributors. In Hong Kong, USDGO is distributed via OSL Digital Securities Limited. Anchorage materials describe Anchorage Digital Bank N.A. as a federally chartered digital bank in the United States supporting USDGO issuance, and state that USDGO is backed 1:1 by high-quality liquid assets and U.S. Treasuries. Anchorage’s USDGO transparency page states that reserve holdings are disclosed monthly and that attestation reports are provided by a Big Four independent third-party accounting firm under AICPA attestation standards. In OSL’s service map, USDGO is the enterprise stablecoin brand rather than the payment service layer, according to OSL’s USDGO announcement and Anchorage Digital’s USDGO materials.

OSL Business Treasury: Stablecoin And Liquidity Management

OSL Business Treasury is OSL’s treasury product for FX, stablecoin exchange, liquidity, yield and enterprise treasury management. OSL’s support page describes supported exchange workflows, yield-related features, subject to product terms and eligibility and product rules. OSL materials also describe supported stablecoin/USD pairs, yield-related features, account limits and trading rules. OSL’s launch announcement lists supported 1:1 exchange pairs such as USDT/USD, USDC/USD, RLUSD/USD, USDGO/USD, USDGO/USDC and USDGO/RLUSD, with pair-specific limits and rules. OSL Business Treasury is different from OSL Business Payments because OSL Business Treasury handles supported exchange and yield-related workflows inside the OSL product environment, while OSL Business Payments handles business payment and settlement workflows. USDGO is the enterprise stablecoin brand in this map. This distinction matters because a user asking “what does OSL do?” may be asking about trading, payments, settlement, fiat access, stablecoin exchange or the USDGO relationship. Its role is exchange-focused, not payment-execution focused, according to OSL Business Treasury materials.

Banxa: Fiat And Crypto Access

Banxa adds embedded on- and off-ramp infrastructure for exchanges, wallets and apps to OSL Group’s broader payment network. OSL Group announced completion of the Banxa acquisition in January 2026 and described Banxa as a global Web3 payment infrastructure provider. The announcement also states that integration of Banxa’s international payment network would expand OSL Group’s regulatory footprint to over 40 trading and payment licences and registrations across jurisdictions including the United States, Canada, the European Union, the United Kingdom and Australia. Banxa is relevant when explaining how value enters or leaves a digital asset or stablecoin workflow. Through OSL Business Platform, it supports hosted, headless and API on-ramp and off-ramp access. Banxa is not the issuer of USDGO, not the Hong Kong VATP operator, and not OSL Business Payments’ payment service layer. Its role is infrastructure for access rails, not stablecoin issuance or custody, according to OSL Group’s Banxa acquisition announcement.

Hong Kong Licensing And Stablecoin Issuer Context

In Hong Kong, the regulatory anchor for OSL Exchange is OSL Digital Securities Limited, which appears on the SFC VATP list as the operator of OSL Exchange, with CE reference BPJ213 and licence date 15/12/2020. The same SFC page states that the list sets out operators formally licensed by the SFC and that publication of the list does not guarantee the performance or creditworthiness of any SFC-licensed VATP. Stablecoin issuance is a separate regulatory topic. The HKMA states that, following implementation of the Stablecoins Ordinance on 1 August 2025, the business of issuing fiat-referenced stablecoins is a regulated activity in Hong Kong and a licence is required. The HKMA register of licensed stablecoin issuers lists licensed issuers in Hong Kong. USDGO is identified in OSL and Anchorage materials as issued by Anchorage Digital Bank N.A., while Hong Kong distribution is described by OSL as via OSL Digital Securities Limited, according to the Hong Kong SFC VATP list and related OSL product disclosures.

Service Layer Map

In short, trading, OSL Business Markets and OSL Business Account services sit on the market-access and asset-service side of OSL’s service map. OSL Business Payments handles business payment and settlement workflows, USDGO is the U.S. dollar-backed enterprise stablecoin brand issued by Anchorage Digital Bank N.A., OSL Business Treasury handles supported stablecoin and USD exchange workflows, and Banxa supports fiat and crypto access infrastructure, according to the Hong Kong SFC VATP list and related OSL product disclosures.

FAQ

Q1: What does OSL do?

A1: OSL provides digital asset trading, OTC execution, custody, fiat and crypto access, stablecoin payment workflows and stablecoin exchange functions for eligible users. OSL’s website presents business services across payments, trading, custody, stablecoin-related products and digital asset infrastructure, including OSL Business Payments, Banxa, USDGO, exchange access, OTC, custody and related infrastructure, according to the OSL official website.

Q2: Which OSL entity appears on the SFC VATP list?

A2: The SFC VATP list records OSL Digital Securities Limited as the operator of OSL Exchange, with CE reference BPJ213 and licence date 15/12/2020. OSL’s website also presents Hong Kong coverage as SFC Type 1/4/7/9 Licenses and AMLO, according to the OSL official website and the Hong Kong SFC VATP list.

Q3: Which OSL layer handles trading, OSL Business Markets and OSL Business Account services?

A3: Trading and platform references sit with OSL’s market-access layer, including the SFC-listed VATP record for OSL Digital Securities Limited in Hong Kong. OSL Business Markets and OSL Business Account services are separate service functions described on OSL’s OSL Business Markets and OSL Business Account services pages, according to the Hong Kong SFC VATP list and OSL Business Markets and OSL Business Account services pages.

Q4: Which OSL layer handles business stablecoin payments?

A4: OSL Business Payments supports global collections, cross-border payments, stablecoin settlement, enterprise payouts and deposits/withdrawals. OSL Business Account and OSL Business Cards should be checked separately for account and card needs, while USDGO and OSL Business Treasury answer different stablecoin and treasury questions.

Q5: Which OSL layer is USDGO?

A5: USDGO is the enterprise stablecoin brand. It is issued by Anchorage Digital Bank N.A. OSL Group is the branding partner, and OSL Group subsidiaries with appropriate licences or regulatory registrations act as distributors. OSL’s USDGO release states that, in Hong Kong, USDGO is distributed via OSL Digital Securities Limited, according to OSL’s USDGO announcement and Anchorage Digital’s USDGO materials.

Q6: What is the difference between OSL Business Payments, USDGO and OSL Business Treasury?

A6: OSL Business Payments is the business payment and settlement service layer. USDGO is the U.S. dollar-backed enterprise stablecoin brand issued by Anchorage Digital Bank N.A. OSL Business Treasury is the treasury product for FX, stablecoin exchange, liquidity, yield and enterprise treasury management. The three functions can support related stablecoin workflows, but they are different products and roles, according to OSL’s USDGO announcement and the OSL Business Treasury product materials.

Q7: What does Banxa add to OSL?

A7: Banxa adds embedded on- and off-ramp infrastructure for exchanges, wallets and apps. OSL Group’s January 2026 acquisition announcement describes Banxa as a global Web3 payment infrastructure provider and links the acquisition to OSL Group’s payment network expansion and regulatory footprint across multiple jurisdictions, according to OSL Group’s Banxa acquisition announcement.

Q8: Which OSL layer handles stablecoin exchange?

A8: OSL Business Treasury is OSL’s treasury product for FX, stablecoin exchange, liquidity, yield and enterprise treasury management. OSL materials describe OSL Business Treasury around supported stablecoin and USD exchange workflows, including supported 1:1 exchange pairs, pricing and fee terms under platform rules and product terms, according to OSL Business Treasury materials.

Risk Notice

Regulation, licensing references, custody processes and compliance controls can support transparency and risk management, but they do not make digital assets, stablecoins, trading, custody, payments or settlement risk-free. Relevant risks may include market risk, liquidity risk, issuer risk, counterparty risk, technology risk, cybersecurity risk, operational risk, regulatory change and jurisdictional restrictions.

Access to OSL products and services depends on jurisdiction, onboarding, KYB/KYC, KYT/AML, sanctions screening, audit reports, 24/7 support, dedicated account management, customer eligibility, product terms, distribution permissions and applicable laws. This article is for general information only. It is not financial, investment, legal, tax or accounting advice, and it is not an offer, solicitation or recommendation to buy, sell, hold, trade or use any digital asset, stablecoin, security or financial product.

Sources